The Trillion Dollar Question

The 12 most valuable companies on earth sell infrastructure. The next one will sell the output.

Sequoia just published one of the most important pieces on AI this year. The thesis is simple. The next trillion dollar company won’t sell software. It will sell the work.

I agree. But I think they’re underselling the shift.

Let me explain why by looking at the companies that already crossed the trillion dollar line. And what they tell us about what comes next.

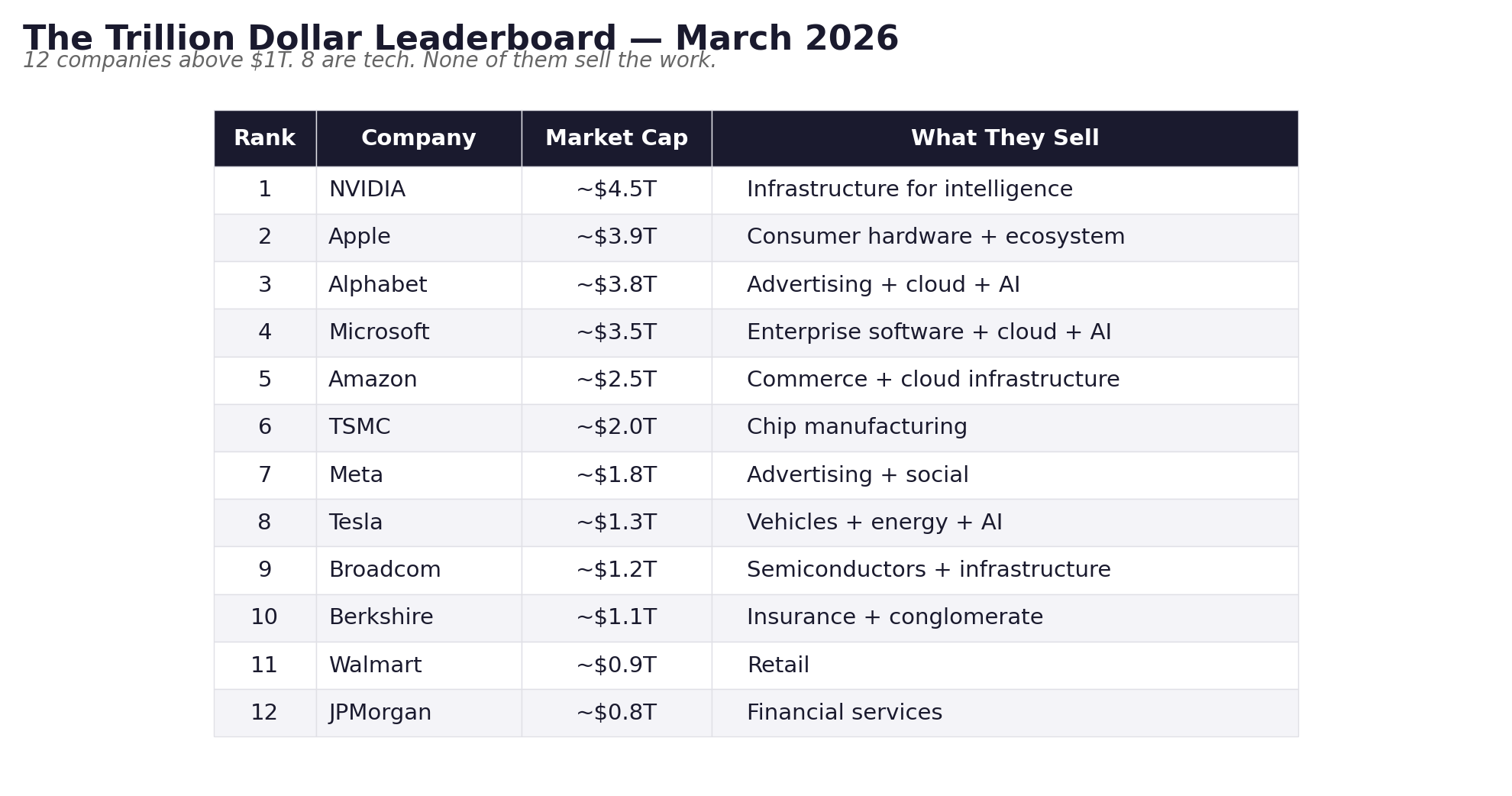

The Leaderboard

Here are the most valuable companies on earth as of March 2026:

Twelve companies around or above a trillion. Eight are tech. Four are semiconductors or semiconductor-adjacent. The pattern is obvious. The market is betting on the infrastructure layer of the intelligence age.

But here is the question nobody is asking loudly enough:

What happens when the infrastructure layer is built?

Software Ate the World. Labor is the World.

There is a reason Sequoia’s piece matters. They put a number on the ratio that changes everything.

For every $1 spent on software, $6 is spent on services.

Let that sit.

Global IT spending in 2026 is projected at $6.15 trillion. Software is about $1.4 trillion of that. The global professional services market alone is over $6 trillion. US wages totaled $11.7 trillion in 2024. Globally, labor compensation runs somewhere north of $40 trillion annually.

The software market is a rounding error compared to the labor market.

Every SaaS company on earth is fighting over the $1. The $6 is wide open. And AI is the first technology in history capable of going after it directly.

Intelligence vs. Judgement

Sequoia’s framework is useful here. They split work into two categories.

Intelligence is rule-based complexity. Translating a spec into code. Processing an insurance claim. Coding a medical bill. The rules are hard but they are rules. AI is already doing this autonomously.

Judgement is pattern recognition built on years of experience. Deciding which feature to build. Knowing when a client relationship is at risk. Reading the room in a negotiation. AI is not there yet. But the frontier is shifting.

The key insight: every profession has a ratio of intelligence to judgement. The higher the intelligence ratio, the sooner AI replaces the worker entirely.

Software engineering got there first. Over half of all AI tool usage across professions is in software engineering. That is not because engineers love tools. It is because writing code is mostly intelligence work.

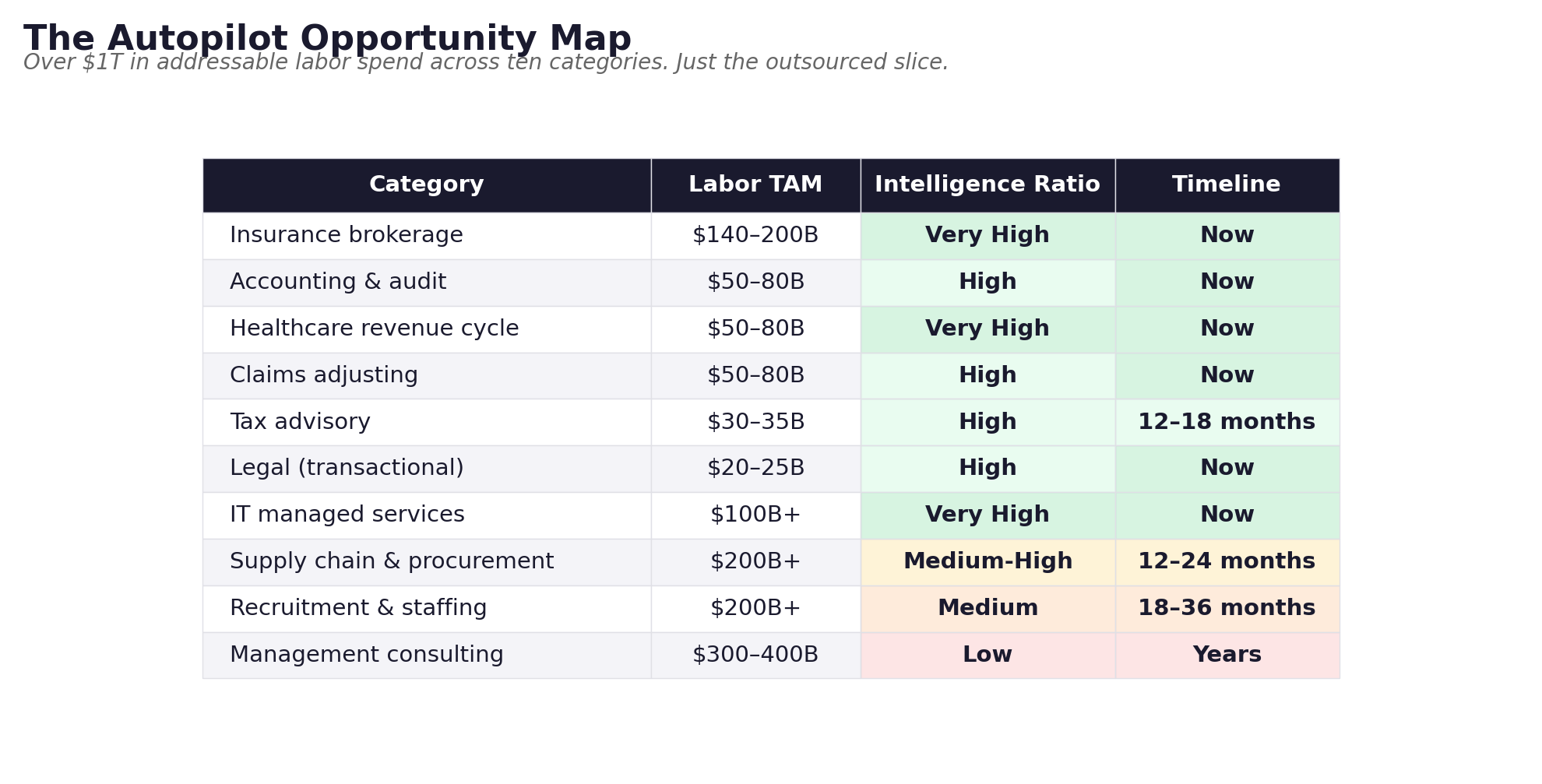

Now look at the rest of the economy through this lens:

Add those up. That is over $1 trillion in addressable labor spend in just ten categories. And that is only the outsourced slice.

What the Top 12 Tell Us

Go back to the leaderboard. Every company above a trillion earned its position by capturing a fundamental economic function.

NVIDIA captured compute. Apple captured the consumer device. Alphabet captured attention. Microsoft captured the enterprise desktop. Amazon captured commerce and cloud. TSMC captured fabrication. Walmart captured retail distribution. JPMorgan captured financial intermediation.

Each of these is a platform that sits between supply and demand for something essential. They did not just build tools. They became the infrastructure through which economic activity flows.

Now apply this to labor.

The companies on this list sell picks and shovels. They sell the infrastructure. They sell the tools. None of them sell the work itself. Not yet.

Microsoft sells Office. It does not close your books. Alphabet sells ads. It does not process your insurance claims. Amazon sells cloud. It does not handle your HR operations.

That gap is the opportunity Sequoia is pointing at.

Copilots vs. Autopilots

Sequoia draws a clean line here.

A copilot sells the tool. It makes the professional more productive. Harvey for lawyers. Rogo for investment bankers. The human stays in the loop. The tool captures the software budget.

An autopilot sells the work. It replaces the professional for a specific task. The customer buys the outcome directly. The autopilot captures the labor budget.

The copilot approach was right when models lacked intelligence. You needed a human to provide judgement. The tool just accelerated their work.

But models are now intelligent enough that for high-intelligence tasks, the human in the loop is the bottleneck.

Copilots compete with other tools. Autopilots compete with headcount.

The tool budget is a $1.4 trillion market. The labor budget is a $40+ trillion market. The math is not close.

The Outsourcing Wedge

Here is the playbook Sequoia outlines, and this is where I think they are exactly right.

Start where outsourcing already exists. If a company already outsources a function, three things are true:

They accept the work can be done externally

There is a budget line that can be swapped cleanly

The buyer is already purchasing an outcome

Replacing an outsourcing contract with an AI-native service provider is a vendor swap. Replacing internal headcount is a reorg. One is a procurement decision. The other is a political crisis.

This is exactly what we see at Humanity Labs. When we walk into a wealth management firm and offer to handle their account transfers, data reconciliation, or client onboarding with digital workers, the first wins come from tasks they already outsource or tasks that simply are not getting done because nobody has the bandwidth.

The tasks nobody has time for are the real wedge. There is no budget line to displace. No incumbent to fight. Just found capacity.

What a Trillion Dollar Labor Company Looks Like

So what does the next trillion dollar company actually look like?

It will not look like Salesforce. It will not look like ServiceNow. It will not even look like Accenture.

It will look like a company that:

Sells outcomes, not seats. Pricing is per task, per FTE equivalent, or per outcome delivered. Not per user per month.

Compounds on data. Every task completed makes the system smarter. Every edge case resolved expands the frontier of what the system can handle autonomously.

Starts in outsourced, intelligence-heavy work. The wedge is specific, measurable, and already budgeted.

Expands into insourced, judgement-heavy work. As the system learns what good judgement looks like in a domain, it moves from doing the intelligence work to doing the full job.

Operates as a service company with software economics. Gross margins north of 80% because AI does the work. But the customer experience feels like hiring a team.

The business model is not SaaS. It is not traditional services. It is something new. It is digital labor sold as a managed service.

The Convergence

Today’s copilots will try to become autopilots. Sequoia says it explicitly. But they also note the innovator’s dilemma: if you sell the tool to the professional, becoming an autopilot means cutting your own customer out of the equation.

Harvey sells to law firms. To become an autopilot, Harvey would need to sell directly to the company that needs the NDA drafted, bypassing outside counsel entirely. That is not a product pivot. That is a go-to-market inversion.

The companies that start as autopilots do not face this problem. They are building the muscle to deliver outcomes from day one. They are accumulating the data on what good work looks like in their domain. They are building trust with the end buyer, not the intermediary.

This is why pure-play autopilots have a structural advantage.

What This Means

The biggest companies in the world got there by becoming essential infrastructure for economic activity. The next wave will get there by becoming essential infrastructure for economic output.

Not tools that help people work. Systems that do the work.

The $6 trillion professional services market is the first addressable target. The $40+ trillion global labor market is the endgame.

The twelve companies above a trillion today built the roads. The next one will drive the trucks.

If you’re building in this space or thinking about the digital workforce shift, I write about it regularly at ap.xyz.