The Expanding Enterprise Stack, Part 1: Humans + Software + Digital Workforces

On Tuesday, a Goldman Sachs basket of software stocks fell 6% in a single session, its worst day since the April tariff shock. The iShares Expanded Tech-Software Sector ETF (IGV) dropped 4.6%. ServiceNow and Salesforce each shed 7%. Intuit collapsed 11%.

On Wednesday, the selling continued. The Nasdaq fell another 2.3%. Palantir dropped 10%. AMD plunged 17%. The S&P 500 lost another 1%.

The two-day rout has now spread globally. Indian IT exporters fell 6.3%. China’s CSI Software Services Index dropped 3%. Hong Kong’s Kingdee tumbled 13%. Japan’s Recruit Holdings and Nomura Research lost 8-9% each.

Bloomberg put the damage at $285 billion wiped out in a single day.

A Jefferies trader called it the “SaaSpocalypse.” His description of the trading: “Get me out.”

After watching this for two days, I wrote this.

A Year in the Making

This week’s carnage is the acceleration of a trend that’s been building for over a year.

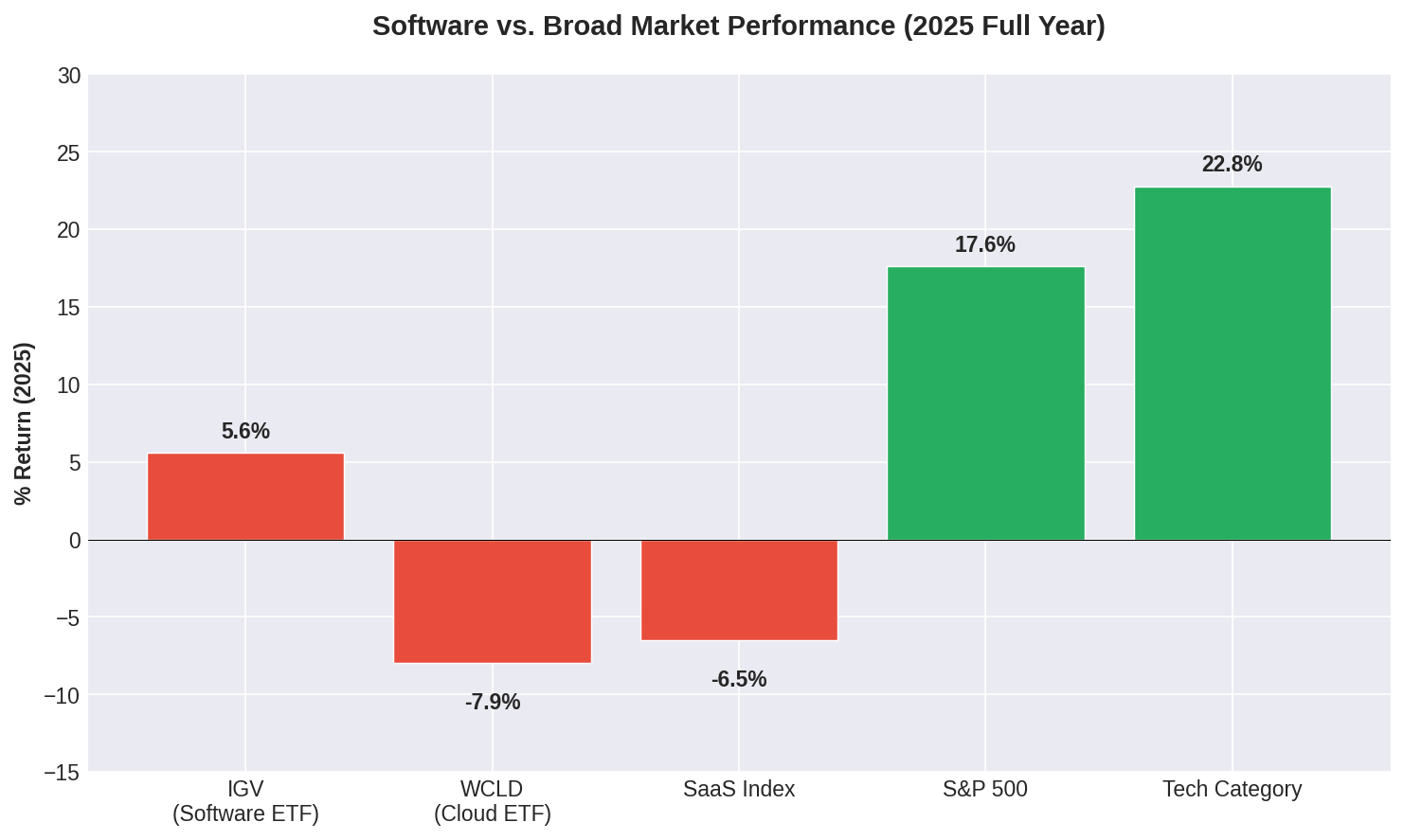

In 2025, IGV returned 5.56% while the broader tech category gained 22.78%. The WisdomTree Cloud Computing Fund (WCLD) posted negative 7.94%. The SaaS Index fell 6.5% while the S&P 500 climbed 17.6%.

The divergence widened into 2026. IGV dropped 16% in January alone. Year-to-date, ServiceNow is down 28%, Salesforce down 26%, Intuit down 34%.

Revenue multiples for SaaS companies have compressed from above 7x at the start of 2025 to below 5x today.

The market is pricing software as if it’s a dying category.

The Trigger and the Thesis

The immediate catalyst was Anthropic releasing a productivity tool for in-house lawyers on Tuesday. But the fear has been building since January’s Claude Cowork launch.

The bear thesis has two parts:

First, that AI coding tools (”vibe coding”) will let enterprises build their own software. Why pay for Salesforce when Claude can build you a CRM?

Second, that AI agents will automate away the workflows that software currently supports. Why buy ServiceNow if an agent handles the ticket routing?

“The draconian view is that software will be the next print media or department stores,” the Jefferies trader told Bloomberg.

Jensen Huang pushed back at a Cisco-hosted AI conference yesterday: “There’s this notion that the tool in the software industry is in decline, and will be replaced by AI. It is the most illogical thing in the world, and time will prove itself.”

The market kept selling anyway.

But Huang’s point deserves deeper analysis than dismissal. He’s making an architectural observation about how enterprise stacks actually work.

The Stack Is Expanding, Not Contracting

For 40 years, the enterprise stack has been simple: Humans + Software

Software amplified human productivity. Humans operated software. The relationship was direct.

What’s emerging now isn’t a replacement of that stack. It’s an expansion: Humans + Software + Digital Workforces

Digital workforces are a new layer. They sit between humans and software, executing at a velocity and scale humans cannot match. But they don’t eliminate the other layers. They increase demands on both.

Digital Workforces Are a Consumption Layer

A digital workforce processing 50,000 client requests per month doesn’t reduce software usage. It multiplies it.

Every automated workflow requires:

Data to read and write

APIs to call

Systems to authenticate against

Audit trails to maintain

Compliance checks to pass

Digital workforces are the largest net-new consumers of software infrastructure in a generation. They’re not replacing Snowflake and Datadog. They’re becoming their biggest customers.

The more work that shifts to digital workforces, the more software those workforces need to operate on.

The New Value Hierarchy

In the expanded stack, value accrues to two things:

Data Networks

Software that accumulates proprietary data through usage becomes exponentially more valuable. Every transaction, every client interaction, every workflow execution adds to a data asset that digital workforces can learn from and operate on.

A CRM with 10 years of client interaction history isn’t threatened by this shift. It’s essential to it. The digital workforce that can access that data network delivers dramatically better outcomes than one starting cold.

More digital workforce activity = more data flowing through these systems = stronger network effects = higher switching costs.

Functions Exposed to Digital Workforces

The second value driver is capability exposure. Software that exposes its functions as callable operations becomes infrastructure for the new layer.

“Generate a proposal” as an API endpoint is valuable. “Generate a proposal” as a 12-step UI wizard is a liability.

Digital workforces don’t browse software. They call functions. Every capability locked behind a GUI is a capability that can’t be leveraged at scale. Every capability exposed as a clean function becomes part of the digital workforce’s toolkit.

Bank of America made a version of this argument yesterday, upgrading SAP amid the carnage: “Deep domain expertise and business integration are hard for new entrants to replicate, making complex, mission-critical platforms like SAP less vulnerable as they embed GenAI using proprietary customer data.”

The platforms that expose rich function libraries will see usage multiply as digital workforces adopt them as core infrastructure.

What This Means for Software Companies

This isn’t about survival. It’s about positioning within the new stack.

Expanding value:

Systems of record with deep data networks

Platforms with clean, comprehensive APIs

Infrastructure software (more digital workforce activity = more infrastructure load)

Workflow engines that can be orchestrated programmatically

Compressing value:

Point solutions with thin data assets

Software where the primary value is the UI

Tools that can’t be called by digital workforces

Anything that requires human-in-the-loop for basic operations

The question for every software company isn’t “will AI replace us?” It’s “are we building for a stack that includes digital workforces, or are we building for a stack that’s going away?”

The Math on the Sell-Off

The market is applying a single narrative (AI replaces software) to a complex reality (AI changes which software wins).

Consider the compression in valuations. SaaS multiples have dropped from 7x+ to below 5x revenue. For companies with strong data networks and API exposure, this represents a mispricing. For point solutions with thin moats and GUI-dependent workflows, it may be generous.

The blunt instrument of sector-wide selling creates opportunities in the former while masking continued risk in the latter.

As one fund manager told reporters this week, there’s a “discrepancy between excellent fundamentals and catastrophic price performance, a phenomenon rarely observed in this form.”

The Expanded Stack Is Larger, Not Smaller

The simplest way to see this: the three-layer stack is bigger than the two-layer stack.

Humans still need software. Now digital workforces also need software. That’s two sources of demand instead of one.

The humans in this stack shift toward judgment, oversight, and exception handling. The digital workforces handle volume and velocity. The software serves both.

Total software consumption goes up. Total value of data networks goes up. Total demand for exposed functions goes up.

The stack isn’t shrinking. It’s expanding. And every layer of it needs software to function.

Great piece — this articulated something I’ve been feeling across the work but hadn’t seen framed this cleanly.

I’m seeing the same expansion you describe from the marketing side of the enterprise stack. I work in AI infrastructure helping teams apply AI across their marketing and GTM systems, and the pace of change has forced me to stay aggressively platform-agnostic. Tools come and go. What sticks is whether a company is becoming AI-native in how it thinks, builds, and communicates.

Where this really resonates is your point that digital workforces are a consumption layer, not a replacement layer. In marketing, every “automated” workflow actually increases demand downstream: more data ingestion, more API calls, more orchestration, more judgment at the edges. The teams that struggle are the ones treating AI as a feature bolt-on. The teams that win are redesigning the stack so AI is embedded in both the product and the messaging layer that sits on top of it.

One counter-insight from the field: companies that talk about being AI-powered before they’ve re-architected internally tend to stall. The most durable players I’m seeing rebuild the stack first, then let the positioning emerge naturally from real capability.

Curious how you’re thinking about this showing up in GTM and customer-facing systems specifically — do you see marketing stacks becoming their own kind of digital workforce, or just the proving ground for the broader shift?