Fat Margins Hide a Lot of Sins

What meatpacking knows about AI that wealth management is still figuring out

A half percent doesn’t sound like much.

Cargill just deployed a computer vision system called CarVe across its beef fabrication lines. Cameras mounted above the production line watch every carcass in real time. They spot leftover red meat on the bones. Each worker gets a green, yellow, or red score after every cut.

The result: roughly 0.5% more yield per animal.

That doesn’t sound like it matters. But Cargill processes 4,000 cattle per day at its Fort Morgan, Colorado plant alone. Across the industry, even a 1% improvement in yield keeps over 200 million additional pounds of beef in the food supply annually. That’s more than a million additional meals from the same number of animals.

Cargill CEO Brian Sikes put it simply: every single ounce of recovered beef equates to roughly 350,000 meals per year across their operations.

Here’s what makes this interesting. It’s not the technology. It’s the economics.

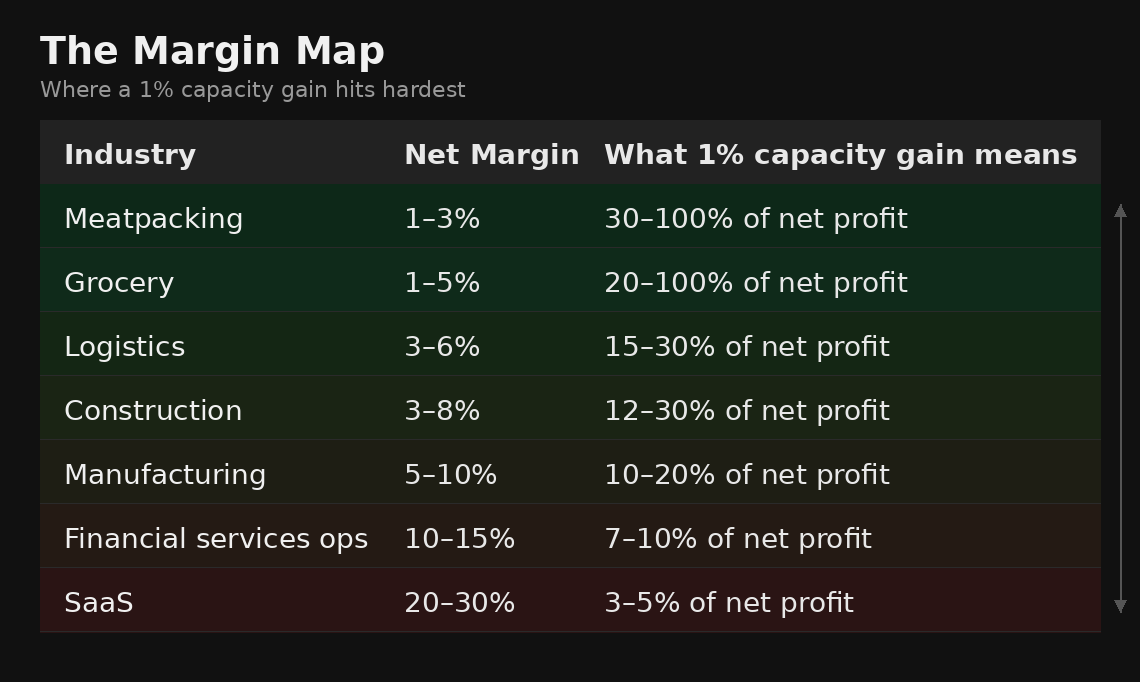

The Margin Map

Meatpacking runs on razor-thin margins. JBS, the world’s largest meat processor, reported EBITDA margins of negative 1.6% in its North American beef division in Q1 2025. Tyson’s operating margin on beef has bounced between 2% and 9% depending on the cattle cycle. When your net margin is 2-3% in a normal year, a 0.5% yield improvement isn’t a nice-to-have. It’s a 15-25% improvement in profitability.

Now compare that to software. SaaS companies run 20-30% net margins. You can have bloated teams, redundant tools, broken processes, and meetings about meetings. The margin absorbs all of it. Nobody notices because the economics are forgiving enough to survive bad execution.

Here’s a rough margin map across industries:

The thinner the margin, the more a fractional capacity gain changes the entire business. The fatter the margin, the more it forgives.

Fat margins hide a lot of sins.

Thin margins hide nothing.

Where AI Is Actually Landing

This is the pattern across every industry where AI is creating measurable, documented value today. Not the industries with the fattest margins. The ones with the thinnest.

Meatpacking. Cargill’s CarVe system. JBS partnering with Völur (a Norwegian AI company) to optimize deboning at one of North America’s most advanced beef plants. Tyson deploying computer vision to automate inventory tracking that was previously done by hand. The whole industry is moving because it has to. U.S. cattle herds are at their lowest level in 70 years. Beef production is expected to drop 5% in 2026. Every ounce matters.

Agriculture. Precision farming has reached an estimated 80% AI adoption rate. Thin margins and weather-dependent operations create existential incentives for optimization. Farmers report 10-20% improvements in crop yields using AI-driven planting, irrigation, and pest detection. But here’s the nuance: a recent Purdue analysis found that most agribusiness firms never scale AI past pilot stage. Thin margins mean you can’t afford to waste money on experiments that don’t work, either.

Manufacturing. 77% of manufacturers now use AI in some form, up from 70% in 2023. The biggest use cases: predictive maintenance, quality control, and supply chain management. Most manufacturers (53%) prefer AI copilots over autonomous systems. They want the tool to make the worker better, not replace the worker. Sound familiar?

Logistics. Net margins of 3-6%, with overhead consuming 83-86% of revenue. AI is deployed for route optimization, demand forecasting, and fleet management. Edge AI is running models directly on trucks and warehouse equipment for real-time decision-making.

Now compare all of that to where most AI dollars are flowing today. Coding tools. Marketing copy. Meeting summarizers. Knowledge management. These are real products solving real problems. But they’re landing in fat-margin industries where the bar is “save people time.” A chatbot that saves a knowledge worker 20 minutes a day is nice. A computer vision system that adds 200 million pounds of beef to the food supply is new capacity. That’s a different category of impact.

Where We Are on the Adoption Curve

The data on this is clear: we are still early.

The U.S. Census Bureau’s Business Trends and Outlook Survey shows AI adoption among U.S. firms has more than doubled in two years, rising from 3.7% in fall 2023 to 9.7% by August 2025. That’s rapid growth. But it means over 90% of U.S. businesses are not yet using AI in production.

The St. Louis Fed pegs overall generative AI usage at 54.6% of adults, up 10 percentage points in the past year. But that’s usage, not deployment. Most of that is individuals using ChatGPT, not companies redesigning workflows.

McKinsey’s 2025 State of AI survey found that 88% of organizations use AI in at least one function. But only 6% qualify as “high performers” who attribute 5%+ EBIT impact to AI. And only 23% are scaling AI agents, mostly in just one or two functions.

The Anthropic Economic Index puts it plainly: enterprise use of AI is growing rapidly, but we are still in the early stages. Usage remains unevenly distributed across the economy.

Here’s the adoption pattern by industry maturity:

Scaled and proving ROI: IT/tech, coding tools, customer service chatbots

Early production, measurable gains: Manufacturing, agriculture, meatpacking, logistics

Piloting but not scaling: Construction, government, legal

Bimodal: Financial services. A handful of firms are deploying AI into live operations. The vast majority are still forming committees.

That gap is the one that should worry people. Not the gap between industries. The gap within them.

The Coaching Model Wins

There’s a second lesson in the Cargill story that most people miss.

They’re not replacing butchers. They’re coaching them.

CarVe gives workers instant feedback. Green, yellow, red. It spots weaknesses on specific fabrication lines so managers can coach individuals instead of yelling at the whole crew. It also catches workers doing a great job and prompts managers to praise them. Cargill’s slaughter manager called the gamification element “truly a game changer.”

This is not altruism. Training a skilled butcher takes months. Turnover in meatpacking is brutal. If you can get more output from your existing workers through real-time AI coaching, that’s worth far more than trying to automate them out. Same people. More capacity.

Cargill’s $90 million Factory of the Future investment includes 100+ automation projects across 35 facilities. But the highest-impact project isn’t a robot. It’s a camera that makes people better at their jobs.

The industries that understand this will win. The ones chasing full automation fantasies will burn capital and end up back where they started.

The Call

We see the discrepancy every week.

Some wealth management firms are already deploying AI into live operations. They’re measuring output in FTEs delivered. They’re not “saving time” on account transfers, client onboarding, and compliance reporting. They’re adding capacity. New work getting done that wasn’t getting done before. They’re past the pilot phase and into production.

Then there’s everyone else. Still debating whether to try a pilot. Still asking vendors for demos. Still forming committees. Still running “AI strategy workshops” that produce slide decks instead of deployed systems.

The back-office work at advisory firms is repetitive, high-volume, and already systematized. These are the exact characteristics that make thin-margin industries successful with AI: clear objectives, measurable outputs, and fast feedback loops. The work is ready. The technology is ready. The question is whether the firms are ready to add capacity instead of just talking about it.

Meanwhile, meatpackers are already in production. Farmers are already in production. Manufacturers are already in production. These industries didn’t wait for perfect conditions. They moved because thin margins gave them no other choice.

Wealth management has fatter margins. That buys time. But time is not the same as advantage. The firms deploying today are adding capacity every quarter. More work done. More clients served. More advisors freed up. The gap between firms that deploy in 2026 and firms that start in 2028 won’t be two years of progress. It will be two years of compounding capacity that the late movers may never close.

Every other thin-margin industry figured this out already. Wealth management has the data, the systems, and the workflows to do the same. The only thing missing is the decision to move.

Fat margins give you the luxury of waiting. They also give you the luxury of falling behind.

Don’t confuse the two.